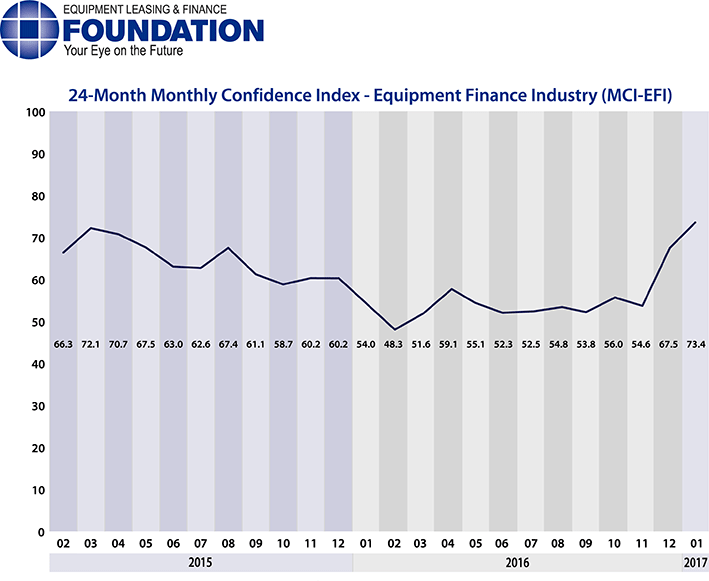

The Equipment Leasing & Finance Foundation (the Foundation) releases the January 2017 Monthly Confidence Index for the Equipment Finance Industry (MCI-EFI) today. Designed to collect leadership data, the index reports a qualitative assessment of both the prevailing business conditions and expectations for the future as reported by key executives from the $1 trillion equipment finance sector. Overall, confidence in the equipment finance market is 73.4, an increase from the December index of 67.5, and the highest index since the MCI was launched in May 2009 to track recovery after the 2008 downturn.

When asked about the outlook for the future, MCI-EFI survey respondent Thomas Jaschik, President, BB&T Equipment Finance, said, “The outlook for U.S. companies has become much more positive since the presidential election. Lower taxes, less regulation and rising interest rates will be the catalyst to spur capital asset acquisitions. This will undoubtedly set the stage for robust equipment finance activity.”

January 2017 Survey Results

The overall MCI-EFI is 73.4, an increase from the December index of 67.5.

- When asked to assess their business conditions over the next four months, 74.2% of executives responding said they believe business conditions will improve over the next four months, an increase from 48.4% in December. 22.6% of respondents believe business conditions will remain the same over the next four months, a decrease from 45.2% in December. 3.2% believe business conditions will worsen, a decrease from 6.5% the previous month.

- 71.0% of survey respondents believe demand for leases and loans to fund capital expenditures (capex) will increase over the next four months, an increase from 38.7% in December. 25.8% believe demand will “remain the same” during the same four-month time period, down from 54.8% the previous month. 3.2% believe demand will decline, down from 6.5% who believed so in December.

- 19.4% of the respondents expect more access to capital to fund equipment acquisitions over the next four months, a decrease from 22.6% who expected more in December. 80.6% of executives indicate they expect the “same” access to capital to fund business, an increase from 77.4% the previous month. None expect “less” access to capital, unchanged from last month.

- When asked, 35.5% of the executives report they expect to hire more employees over the next four months, a decrease from 41.9% in December. 61.3% expect no change in headcount over the next four months, an increase from 48.4% last month. 3.2% expect to hire fewer employees, down from 9.7% in December.

- None of the leadership evaluate the current U.S. economy as “excellent,” unchanged from last month. 100.0% of the leadership evaluate the current U.S. economy as “fair,” and none evaluate it as “poor,” both also unchanged from December.

- 61.3% of the survey respondents believe that U.S. economic conditions will get “better” over the next six months, a decrease from 71% in December. 38.7% of survey respondents indicate they believe the U.S. economy will “stay the same” over the next six months, an increase from 25.8% the previous month. None believe economic conditions in the U.S. will worsen over the next six months, a decrease from 3.2% who believed so last month.

- In January, 58.1% of respondents indicate they believe their company will increase spending on business development activities during the next six months, an increase from 48.4% in December. 41.9% believe there will be “no change” in business development spending, a decrease from 51.6% the previous month. None believe there will be a decrease in spending, unchanged from last month.

Survey Demographics

Market Segment:

- Bank: 71.0%

- Captive: 6.5%

- Financial Services: 3.2%

- Independent: 19.4%

- Other: 0.0%

Market Segments Based on Transaction Size of New Business Volume

- Large-Ticket (New Business Volume Avg. Transaction Size Over $5 Million): 19.4%

- Middle-Ticket (New Business Volume Avg. Transaction Size of $250,000 – $5 Million): 38.7%

- Small-Ticket (New Business Volume Avg. Transaction Size of $25,000 – $249,999): 41.09%

- Micro-Ticket (New Business Volume Avg. Transaction Less Than $25,000): 0.0%

Organization Size:

- Under $50 Million: 6.5%

- $50 Million – $250 Million: 16.1%

- $250 Million – $1 Billion: 29.0%

- Over $1 Billion: 48.4%

January 2017 Survey Comments from Industry Executive Leadership

Depending on the market segment they represent, executives have differing points of view on the current and future outlook for the industry.

Bank, Small Ticket

“December new business volume and opportunity pipeline growth indicate increased capital investment activity and utilization of financing for acquisition. I view the rising rate environment as a positive indication and a shift from stagnation to a more normal economic cycle.” Robert Boyer, President, Susquehanna Commercial Finance, Inc.

Independent, Small Ticket

“Small business confidence is very high and we are optimistic that this will equate to more demand for capital expenditures. Hopefully, tax reform doesn’t create too much uncertainty.” David T. Schaefer, CEO, Mintaka Financial, LLC

Bank, Middle Ticket

“We continue to manage through a down cycle in the agriculture industry. We expect the cycle to bottom out in 2017, but do not expect improvement until mid-year 2018 or later. We continue to serve our mission and provide options to customers to help them work through the cycle.” Michael Romanowski, President, Farm Credit Leasing Services Corporation

Bank, Large Ticket

“Hope centers around regulatory reform in Washington. Concerns include the rise in the dollar, which could impact exports.” Thomas Partridge, President, Fifth Third Equipment Finance

Back to Top